Financial Planning

Financial Planning, Forecasting & Reporting

Modern day Financial Planning and Analysis (FP&A) systems integrate with spreadsheets and formulate financial profitability strategies extending beyond the fiscal year. Modern solutions leverage AI-enhanced financial projections and generate enlightening data visualizations. Fostering unity among income statements, balance sheets, and cash flow through the implementation of FP&A software solutions where one can analyze extensive historical and prospective financial statements in real-time from diverse sources within a unified platform.

Benefits

Attain instant access to real-time operational data during a collaborative, strategic planning process. FP&A teams can capitalize on emerging opportunities by maintaining a uniform perspective on workflows and automation processes.

Offer swift and precise financial analysis and counsel to business leaders.

Anticipate the repercussions of potential decisions on cash flow and profitability.

Evaluate and oversee the company’s overall financial well-being and investments.

Develop and sustain detailed financial models and forecasts.

Formulate flexible, integrated financial plans accommodating various scenarios.

Workflow design with departments to compile and consolidate budgets

Align corporate strategy with execution and monitor performance.

Identify and evaluate new revenue opportunities and risks, among other responsibilities.

Our Business Partners In Financial Planning & Analysis

Multi-Dimensional Planning

Enables users to model and analyze data across multiple dimensions, providing a holistic view of business performance.

Scenario Planning

Facilitates the creation of various planning scenarios, helping organizations evaluate different business strategies and potential outcomes.

Collaborative Planning and Workflows

Supports collaborative planning processes, allowing teams across departments to work together on planning, budgeting, and forecasting activities.

Excel Integration

Provides integration with Microsoft Excel, allowing users to leverage familiar Excel interfaces while benefiting from the power of Planning Analytics.

Dynamic Reporting and Dashboards

Enables the creation of dynamic reports and dashboards to visualize key performance indicators (KPIs) and monitor organizational performance.

Security and Governance

Implements robust security measures and governance protocols to ensure data integrity and compliance with regulatory requirements.

Predictive Analytics

Incorporates predictive analytics capabilities, allowing users to forecast future trends and outcomes based on historical data.

Data Integration

Integrates seamlessly with various data sources, enabling users to pull in data from different systems for a unified view of information. Utilizes in-memory processing technology for fast and efficient analysis of large datasets, enabling quick decision-making.

Enroll for

Use Cases & Industry

Dive into the FP&A use cases by Industry to learn about industry-specific solutions. Our Industries Page is a gateway to discovering how we impact businesses across various sectors. Explore the depth of our expertise, tailored services, and success stories that showcase the transformative impact we bring to different industries. Read the following FP&A success stories to see how our chosen technologies are used to create maximum value.

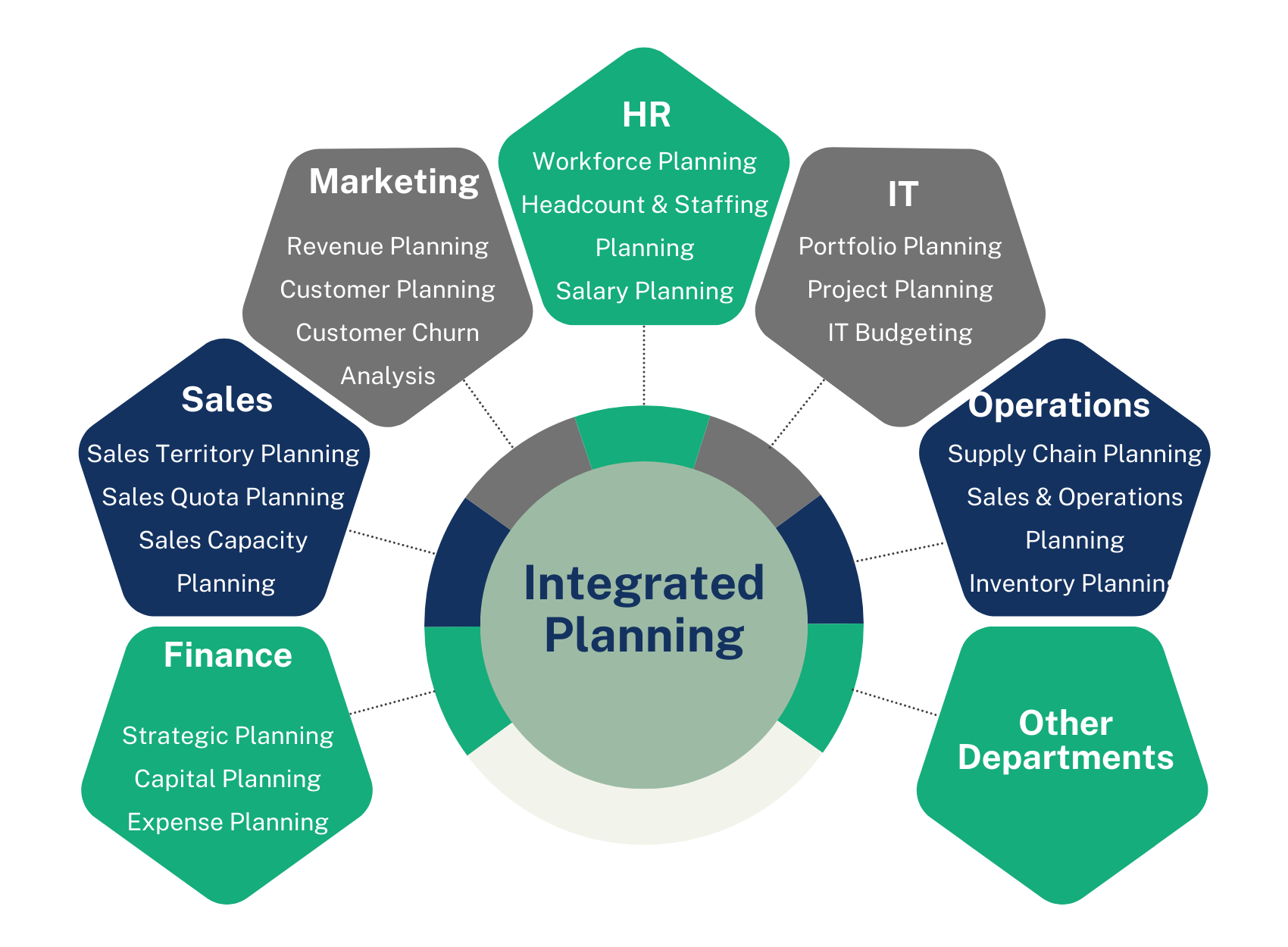

Finance

Surpass the constraints of manual planning by streamlined, integrated financial planning and analysis. Attain alignment between income statements, balance sheets, etc.

Sustainability

Engage in sustainability planning, simulation, and optimization at any level of granularity—including the calculation of the Product Carbon Footprint (PCF)

Supply Chain

Integrate advanced analytics hierarchy and an infinite sandbox for "what-if" analysis into your supply chain operations. Pivoting swiftly transforms disruptions into opportunities.

Workforce

Streamline and automate HR management processes, encompassing employment, salary, bonuses, headcounts, and benefits planning, all within a unified platform. Utilize precise AI-guided workforce plans and forecasts, considering factors like staffing changes, location adjustments, return-to-work scenarios, remuneration variations, etc.

Sales

Monitor and assess real-time sales representative performance and sales capacity data. Harness the capabilities of AI to optimize sales processes, boost productivity, and achieve revenue targets. Automate resource allocation and territory planning for a competitive edge and increased market share

Resources

First Bank Texas

First Bank Texas realized that its financial planning processes relied on the experience and insight of key team members. To develop a more robust planning capability, the bank implemented IBM® Planning Analytics, which streamlines the generation of budgets, financial statements, cash flow reporting and trend analysis.

Liberty Mutual

Discover how Liberty Mutual personalized its employee benefits process to provide more choices, greater transparency and cost-saving opportunities to help employees find their best-fit benefits plans.

knowis AG

German software vendor knowis worked with IBM to use the IBM Db2 on Cloud database to support its financial application, giving its customers a lower cost, lower maintenance deployment option, while increasing knowis’ potential customer base.

Avanse Financial Services Limited

A new-age, education-focused NBFC, Avanse Financial Services Ltd is on a mission to provide seamless and affordable education financing to every deserving Indian student. With a vision to establish itself as a customer-centric digitally agile NBFC, Avanse was seeking to move its complete infrastructure to the cloud that would allow it to scale up easily.

Enento Group

How does the #1 credit info provider in the Nordics inform better financial decisions in real time? It uses Instana to ensure application performance and uptime.

DZee Healthcare Financial Solutions

A healthcare benefits decision support company applies data analytics and machine learning to help employers, benefits advisors and individuals optimize their healthcare plans and reduce their spending.

Visit Cresco's

Featured Blogs

Finance Analytics with IBM Cognos TM1

FAQs

Flat files, such as spreadsheets, word docs, budgeting and forecasting applications, as well as ERP, CRM and any API can be integrated by IBM Planning Analytics with Watson.

Depending on your company’s demands and requirements, the installation procedure can take between 8 weeks to several months.

The engine, a multidimensional database with a cell-oriented layout similar to spreadsheets, is at the heart of IBM Planning Analytics. Its cells are linked to the underlying database via your formulas. All of Excel’s data visualization and analysis capabilities are available in a centralized platform.

Absolutely. You can get Workday Adaptive Planning whether you have another Workday application or not. Our software works with any ERP/GL or other enterprise system (e.g. HR, CRM, Capital, etc.).

Workday Adaptive Planning is designed to support even the most complex planning requirements—so it can work for any organization. We have customers across all industries, geographies, and company size.

Yes. We acquired Adaptive Insights in 2018 and it’s now Workday Adaptive Planning. As part of the Workday enterprise management cloud, Workday Adaptive Planning continues to deliver the best-in-class enterprise planning solution to our thousands of customers.

FP&A is a function within organizations responsible for financial planning, budgeting, forecasting, and analysis. It involves assessing past performance, developing future financial plans, and providing insights to support decision-making.

Key responsibilities of FP&A professionals include budgeting and forecasting, financial modeling, variance analysis, management reporting, providing strategic financial insights, and supporting decision-making across the organization.

While traditional accounting focuses on historical financial reporting and compliance, FP&A is forward-looking and involves forecasting, budgeting, and providing strategic insights to drive decision-making and performance improvement.

A strong FP&A function can lead to improved financial decision-making, better resource allocation, enhanced business performance, increased profitability, and improved stakeholder confidence.

Common tools and technologies used in FP&A include financial planning software, enterprise performance management (EPM) systems, business intelligence (BI) tools, data visualization platforms, and advanced analytics software.

FP&A contributes to strategic planning by providing financial insights and analysis that help align financial goals with overall business objectives, identify growth opportunities, assess risks, and develop actionable plans to achieve strategic targets.

Challenges faced by FP&A professionals include data quality issues, limited access to relevant data, reliance on manual processes, complexity in financial modeling, changing regulatory requirements, and the need to adapt to evolving business conditions.

FP&A supports decision-making by providing accurate and timely financial information, conducting scenario analysis, identifying key performance indicators (KPIs), evaluating investment opportunities, and assessing the financial impact of strategic initiatives.

FP&A plays a critical role in performance management by setting performance targets, monitoring actual performance against targets, analyzing variances, identifying areas for improvement, and recommending corrective actions to drive performance improvement.

FP&A can add value to business operations by providing insights into cost optimization opportunities, revenue growth strategies, investment decisions, resource allocation, pricing strategies, and overall business performance improvement initiatives.

FP&A is the process of analyzing financial data, forecasting future performance, and making strategic decisions to achieve financial goals within an organization.

FP&A helps organizations make informed decisions by providing insights into financial performance, identifying trends, and forecasting future outcomes. It also aids in budgeting, resource allocation, and strategic planning.

Key components include budgeting, forecasting, variance analysis, financial modeling, scenario planning, and strategic decision support.

Common tools include Excel, financial planning software (such as Adaptive Insights or Anaplan), business intelligence software (such as Tableau or Power BI), and enterprise resource planning (ERP) systems.

Financial forecasts are typically created by analyzing historical data, identifying trends, considering external factors (such as market conditions and economic indicators), and applying assumptions to project future financial performance.

FP&A provides insights into the financial implications of different strategic options, helps assess risks and opportunities, and guides resource allocation to support the organization’s overall goals and objectives.

FP&A can help forecast cash flows, identify potential cash flow gaps, optimize working capital, and develop strategies to manage cash effectively, such as monitoring receivables and payables, and optimizing inventory levels.

Best practices include aligning FP&A processes with strategic goals, using accurate and reliable data, involving stakeholders across the organization, continuously monitoring and adjusting plans, and leveraging technology to streamline processes and improve insights.

A balance sheet is a financial statement that summarizes a company’s assets, liabilities and shareholders’ equity at a specific point in time. It provides a snapshot of a company’s financial position, showing what it owns and owes.

A budget spreadsheet is a digital document used to track income, expenses, and spending goals over a defined period. A budget planner is a tool, often incorporating a spreadsheet, that allows you to plan budgets over various timeframes and model different budget scenarios.

The key elements of budgeting include identifying all sources of income, estimating expenses, setting savings goals, comparing estimated numbers to actual figures, making adjustments, and reviewing/revising budgets periodically. Effective budgeting requires planning, prioritizing, and managing spending.

A cash flow report provides the inflows and outflows of cash within a business over a specific time period. It shows how much cash is available for paying expenses, debts, and growth opportunities. Key information includes operating, investing and financing cash flows.

FP&A stands for “Financial Planning & Analysis.” It refers to various processes designed to help business leaders make more informed financial decisions.

The three main financial statements important for FP&A are: 1) Income Statement 2) Balance Sheet 3) Cash Flow Statement. Analyzing these statements helps with budgeting, forecasting, reporting, strategy, and decision making.

Best practices for financial reporting include reporting accurate numbers in a timely manner, maintaining transparency, providing context and analysis for the data, ensuring consistency across reporting periods, following reporting standards/regulations, and communicating findings clearly to stakeholders.

A forecast is an estimate of future financial outcomes based on past performance, current operations, and expectations of economic conditions. A projection is hypothetical estimate based on a set of key assumptions and scenarios. Forecasts inform budgets; projections model possible outcomes.

Examples of financial statements prepared using the FP&A process include cash flow statements, income statements, balance sheets, statements of retained earnings, statements of shareholders’ equity, and statements of cash flows.

A profit and loss (P&L) statement shows a company’s revenues, expenses, and net income or net loss over a specified time period. It provides an overview of operating performance and is one of the key financial statements used in FP&A.

Zero-based budgeting is when budgets are created from scratch each new period, regardless of whether the cost was budgeted in a prior period. All expenses must be approved and justified as though the activities are brand new.

An income statement outlines all revenues generated and expenses incurred over a period. It shows whether a company made a profit or loss during that time. Reviewing statements over sequential periods highlights sales and profitability trends.

A trial balance ensures debits equal credits across general ledger accounts, while a balance sheet is a financial statement summarizing assets, liabilities, and equity on a specific date. The balance sheet allows analysis of financial position; a trial balance checks accounting accuracy.

Best practices include basing assumptions on historical data/trends, accounting for known variables like seasonality, incorporating different growth scenarios, involving various stakeholders, frequently reviewing and updating forecasts, documenting methodology, and clearly communicating limitations.

Power BI can improve FP&A processes by:

- Enhancing data visualization: Create interactive dashboards and reports for easier understanding of financial data.

- Improving collaboration: Share reports and insights with stakeholders across the organization.

- Facilitating scenario planning and forecasting: Analyze different scenarios and predict future financial performance.

TM1, now known as IBM Planning Analytics, is a software platform designed for planning, budgeting, forecasting, and reporting. It allows users to create models, analyze data, and collaborate to make informed financial decisions.

- Improved planning accuracy: TM1 provides tools for scenario planning and what-if analysis, allowing users to test different assumptions and improve the accuracy of their plans.

- Increased efficiency: TM1 centralizes data and streamlines the planning process, saving time and effort.

- Enhanced collaboration: TM1 facilitates collaboration among different departments and stakeholders, ensuring everyone is working with the same data and assumptions.

- Better decision-making: TM1 provides insights and improves visibility into financial data, leading to better decision-making at all levels.

There are many resources available to learn more about TM1, including:

- Cresco University

- IBM Planning Analytics documentation: https://www.ibm.com/support/pages/planning-analytics-documentation

- Online courses and tutorials: Several online courses and tutorials are available to learn TM1 basics and advanced functionalities.

- TM1 user communities: Join online communities and forums to connect with other TM1 users and learn from their experiences.